What Does A Change In Monetary Policy Affect

Affiliate 28. Monetary Policy and Depository financial institution Regulation

28.4 Monetary Policy and Economic Outcomes

Learning Objectives

Past the stop of this section, yous volition be able to:

- Contrast expansionary monetary policy and contractionary monetary policy

- Explicate how monetary policy impacts involvement rates and aggregate need

- Evaluate Federal Reserve decisions over the last forty years

- Explain the significance of quantitative easing (QE)

A budgetary policy that lowers interest rates and stimulates borrowing is known equally an expansionary budgetary policy or loose budgetary policy. Conversely, a budgetary policy that raises interest rates and reduces borrowing in the economy is a contractionary monetary policy or tight monetary policy. This module volition discuss how expansionary and contractionary budgetary policies impact interest rates and amass demand, and how such policies will affect macroeconomic goals like unemployment and inflation. We will conclude with a look at the Fed's budgetary policy practice in contempo decades.

The Effect of Monetary Policy on Interest Rates

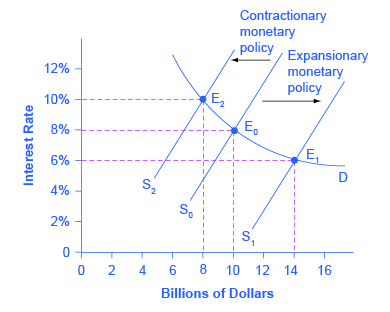

Consider the market place for loanable depository financial institution funds, shown in Figure 1. The original equilibrium (E0) occurs at an interest rate of viii% and a quantity of funds loaned and borrowed of $10 billion. An expansionary budgetary policy will shift the supply of loanable funds to the right from the original supply curve (S0) to Southwardane, leading to an equilibrium (E1) with a lower interest charge per unit of half dozen% and a quantity of funds loaned of $14 billion. Conversely, a contractionary monetary policy volition shift the supply of loanable funds to the left from the original supply curve (S0) to S2, leading to an equilibrium (Eastward2) with a college involvement rate of x% and a quantity of funds loaned of $8 billion.

So how does a central banking concern "raise" interest rates? When describing the monetary policy deportment taken by a fundamental depository financial institution, it is common to hear that the central bank "raised interest rates" or "lowered involvement rates." We need to be clear nearly this: more than precisely, through open market operations the central bank changes bank reserves in a way which affects the supply curve of loanable funds. As a result, interest rates change, as shown in Effigy one. If they do not meet the Fed's target, the Fed tin can supply more or less reserves until interest rates practise.

Recall that the specific interest rate the Fed targets is the federal funds charge per unit. The Federal Reserve has, since 1995, established its target federal funds rate in advance of any open up market operations.

Of class, financial markets display a wide range of interest rates, representing borrowers with different take a chance premiums and loans that are to be repaid over different periods of time. In general, when the federal funds charge per unit drops substantially, other interest rates drib, too, and when the federal funds charge per unit rises, other interest rates rise. However, a fall or rise of ane percentage point in the federal funds rate—which remember is for borrowing overnight—will typically accept an outcome of less than one percentage bespeak on a 30-year loan to purchase a firm or a iii-year loan to purchase a auto. Monetary policy can push the entire spectrum of interest rates higher or lower, but the specific interest rates are ready by the forces of supply and demand in those specific markets for lending and borrowing.

The Effect of Monetary Policy on Aggregate Demand

Monetary policy affects involvement rates and the bachelor quantity of loanable funds, which in plough affects several components of aggregate demand. Tight or contractionary budgetary policy that leads to higher interest rates and a reduced quantity of loanable funds will reduce two components of aggregate demand. Business investment will decline because it is less bonny for firms to infringe money, and fifty-fifty firms that have money will detect that, with higher interest rates, it is relatively more attractive to put those funds in a financial investment than to make an investment in physical capital letter. In addition, higher involvement rates volition discourage consumer borrowing for big-ticket items like houses and cars. Conversely, loose or expansionary monetary policy that leads to lower interest rates and a higher quantity of loanable funds will tend to increase business organisation investment and consumer borrowing for big-ticket items.

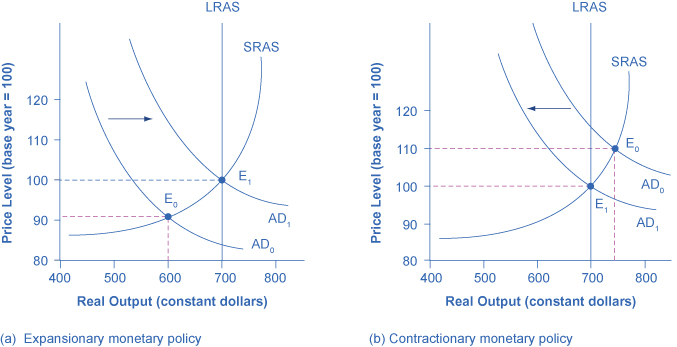

If the economy is suffering a recession and loftier unemployment, with output below potential Gross domestic product, expansionary budgetary policy can help the economy return to potential GDP. Effigy two (a) illustrates this situation. This example uses a brusk-run up-sloping Keynesian aggregate supply curve (SRAS). The original equilibrium during a recession of E0 occurs at an output level of 600. An expansionary budgetary policy will reduce interest rates and stimulate investment and consumption spending, causing the original aggregate need curve (Advertizement0) to shift right to ADi, then that the new equilibrium (E1) occurs at the potential Gross domestic product level of 700.

Conversely, if an economy is producing at a quantity of output above its potential Gdp, a contractionary monetary policy tin reduce the inflationary pressures for a rising price level. In Figure 2 (b), the original equilibrium (E0) occurs at an output of 750, which is higher up potential Gross domestic product. A contractionary monetary policy will raise interest rates, discourage borrowing for investment and consumption spending, and cause the original demand bend (Advertisement0) to shift left to AD1, so that the new equilibrium (E1) occurs at the potential Gdp level of 700.

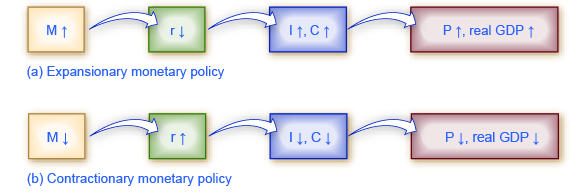

These examples advise that budgetary policy should be countercyclical; that is, information technology should act to counterbalance the business cycles of economic downturns and upswings. Monetary policy should be loosened when a recession has caused unemployment to increase and tightened when inflation threatens. Of class, countercyclical policy does pose a danger of overreaction. If loose budgetary policy seeking to end a recession goes too far, it may push aggregate need so far to the right that it triggers inflation. If tight monetary policy seeking to reduce inflation goes also far, it may push aggregate demand so far to the left that a recession begins. Effigy 3 (a) summarizes the chain of effects that connect loose and tight budgetary policy to changes in output and the cost level.

Federal Reserve Actions Over Last Four Decades

For the period from the mid-1970s up through the end of 2007, Federal Reserve budgetary policy can largely exist summed up by looking at how information technology targeted the federal funds involvement rate using open up market operations.

Of class, telling the story of the U.S. economy since 1975 in terms of Federal Reserve actions leaves out many other macroeconomic factors that were influencing unemployment, recession, economic growth, and aggrandizement over this time. The nine episodes of Federal Reserve action outlined in the sections below also demonstrate that the central banking company should exist considered one of the leading actors influencing the macro economy. Every bit noted earlier, the single person with the greatest ability to influence the U.S. economic system is probably the chairperson of the Federal Reserve.

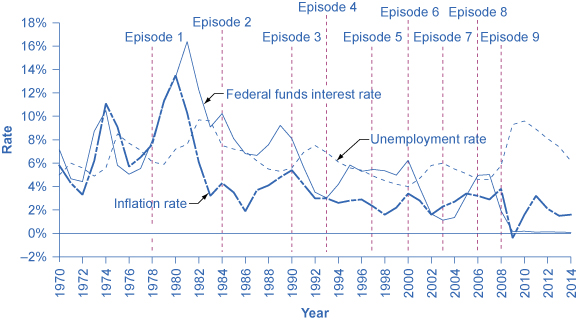

Figure 4 shows how the Federal Reserve has carried out monetary policy by targeting the federal funds interest charge per unit in the last few decades. The graph shows the federal funds involvement rate (remember, this involvement rate is set up through open market operations), the unemployment charge per unit, and the inflation rate since 1975. Unlike episodes of monetary policy during this period are indicated in the figure.

Episode 1

Consider Episode ane in the late 1970s. The charge per unit of inflation was very loftier, exceeding ten% in 1979 and 1980, so the Federal Reserve used tight budgetary policy to heighten interest rates, with the federal funds rate rising from five.5% in 1977 to 16.four% in 1981. Past 1983, inflation was down to 3.2%, but aggregate demand contracted sharply enough that dorsum-to-back recessions occurred in 1980 and in 1981–1982, and the unemployment rate rose from v.8% in 1979 to 9.seven% in 1982.

Episode 2

In Episode two, when the Federal Reserve was persuaded in the early 1980s that inflation was declining, the Fed began slashing interest rates to reduce unemployment. The federal funds interest charge per unit vicious from 16.4% in 1981 to 6.8% in 1986. By 1986 or so, inflation had fallen to well-nigh 2% and the unemployment rate had come up downwardly to 7%, and was still falling.

Episode iii

However, in Episode 3 in the late 1980s, inflation appeared to be creeping upwards again, rising from 2% in 1986 up toward 5% by 1989. In response, the Federal Reserve used contractionary monetary policy to raise the federal funds rates from 6.vi% in 1987 to 9.2% in 1989. The tighter monetary policy stopped inflation, which fell from above 5% in 1990 to under iii% in 1992, but it also helped to cause the recession of 1990–1991, and the unemployment rate rose from 5.3% in 1989 to 7.5% by 1992.

Episode 4

In Episode four, in the early 1990s, when the Federal Reserve was confident that inflation was back under command, it reduced involvement rates, with the federal funds interest rate falling from 8.1% in 1990 to 3.five% in 1992. As the economy expanded, the unemployment rate declined from 7.5% in 1992 to less than v% by 1997.

Episodes v and 6

In Episodes v and vi, the Federal Reserve perceived a gamble of inflation and raised the federal funds rate from iii% to 5.8% from 1993 to 1995. Inflation did not rise, and the period of economic growth during the 1990s continued. Then in 1999 and 2000, the Fed was concerned that inflation seemed to be creeping up and so it raised the federal funds involvement charge per unit from 4.6% in December 1998 to 6.v% in June 2000. Past early 2001, inflation was declining once more, but a recession occurred in 2001. Between 2000 and 2002, the unemployment rate rose from 4.0% to v.8%.

Episodes vii and 8

In Episodes 7 and 8, the Federal Reserve conducted a loose monetary policy and slashed the federal funds charge per unit from half-dozen.two% in 2000 to just 1.7% in 2002, and then again to i% in 2003. They really did this because of fear of Japan-style deflation; this persuaded them to lower the Fed funds further than they otherwise would have. The recession ended, simply, unemployment rates were slow to turn down in the early 2000s. Finally, in 2004, the unemployment charge per unit declined and the Federal Reserve began to raise the federal funds rate until it reached 5% by 2007.

Episode 9

In Episode ix, as the Corking Recession took concur in 2008, the Federal Reserve was quick to slash interest rates, taking them downwardly to ii% in 2008 and to nearly 0% in 2009. When the Fed had taken interest rates downwardly to near-zero by December 2008, the economy was all the same deep in recession. Open market operations could not brand the interest charge per unit plow negative. The Federal Reserve had to think "exterior the box."

Quantitative Easing

The most powerful and commonly used of the three traditional tools of monetary policy—open marketplace operations—works by expanding or contracting the coin supply in a way that influences the interest rate. In belatedly 2008, as the U.S. economic system struggled with recession, the Federal Reserve had already reduced the interest rate to near-null. With the recession notwithstanding ongoing, the Fed decided to adopt an innovative and nontraditional policy known as quantitative easing (QE). This is the purchase of long-term regime and private mortgage-backed securities past central banks to make credit bachelor so as to stimulate aggregate need.

Quantitative easing differed from traditional monetary policy in several central ways. First, it involved the Fed purchasing long term Treasury bonds, rather than short term Treasury bills. In 2008, yet, it was impossible to stimulate the economy any further by lowering brusk term rates considering they were already as low every bit they could get. (Read the closing Bring it Home feature for more than on this.) Therefore, Bernanke sought to lower long-term rates utilizing quantitative easing.

This leads to a second way QE is dissimilar from traditional monetary policy. Instead of purchasing Treasury securities, the Fed also began purchasing private mortgage-backed securities, something it had never washed before. During the fiscal crisis, which precipitated the recession, mortgage-backed securities were termed "toxic avails," because when the housing market collapsed, no one knew what these securities were worth, which put the financial institutions which were holding those securities on very shaky ground. By offering to purchase mortgage-backed securities, the Fed was both pushing long term interest rates downwards and too removing possibly "toxic assets" from the residue sheets of private financial firms, which would strengthen the financial system.

Quantitative easing (QE) occurred in iii episodes:

- During QE1, which began in Nov 2008, the Fed purchased $600 billion in mortgage-backed securities from government enterprises Fannie Mae and Freddie Mac.

- In November 2010, the Fed began QE2, in which it purchased $600 billion in U.South. Treasury bonds.

- QE3, began in September 2012 when the Fed commenced purchasing $twoscore billion of additional mortgage-backed securities per month. This amount was increased in Dec 2012 to $85 billion per month. The Fed stated that, when economic conditions permit, it will begin tapering (or reducing the monthly purchases). Past October 2014, the Fed had announced the terminal $15 billion purchase of bonds, catastrophe Quantitative Easing.

The quantitative easing policies adopted by the Federal Reserve (and by other central banks around the world) are unremarkably thought of as temporary emergency measures. If these steps are, indeed, to exist temporary, and then the Federal Reserve will need to stop making these additional loans and sell off the financial securities it has accumulated. The concern is that the procedure of quantitative easing may testify more difficult to contrary than it was to enact. The testify suggests that QEane was somewhat successful, but that QEtwo and QE3 accept been less then.

Key Concepts and Summary

An expansionary (or loose) monetary policy raises the quantity of money and credit above what information technology otherwise would have been and reduces involvement rates, boosting aggregate demand, and thus countering recession. A contractionary monetary policy, also called a tight monetary policy, reduces the quantity of money and credit below what information technology otherwise would have been and raises involvement rates, seeking to concur down inflation. During the 2008–2009 recession, central banks around the globe as well used quantitative easing to expand the supply of credit.

Self-Check Questions

- Why does contractionary monetary policy cause interest rates to rise?

- Why does expansionary monetary policy causes interest rates to drop?

Review Questions

- How do the expansionary and contractionary monetary policy affect the quantity of money?

- How do tight and loose monetary policy affect involvement rates?

- How practise expansionary, tight, contractionary, and loose monetary policy affect aggregate need?

- Which kind of budgetary policy would you lot expect in response to high inflation: expansionary or contractionary? Why?

- Explain how to utilise quantitative easing to stimulate aggregate demand.

Disquisitional Thinking Questions

A well-known economic model chosen the Phillips Curve (discussed in The Keynesian Perspective chapter) describes the short run tradeoff typically observed between inflation and unemployment. Based on the give-and-take of expansionary and contractionary monetary policy, explain why i of these variables usually falls when the other rises.

Glossary

- contractionary budgetary policy

- a monetary policy that reduces the supply of coin and loans

- countercyclical

- moving in the opposite direction of the business concern cycle of economic downturns and upswings

- expansionary budgetary policy

- a monetary policy that increases the supply of money and the quantity of loans

- federal funds rate

- the interest rate at which one banking company lends funds to some other bank overnight

- loose budgetary policy

- see expansionary budgetary policy

- quantitative easing (QE)

- the purchase of long term regime and individual mortgage-backed securities past key banks to make credit available in hopes of stimulating aggregate need

- tight monetary policy

- run across contractionary monetary policy

Solutions

Answers to Self-Bank check Questions

- Contractionary policy reduces the corporeality of loanable funds in the economy. As with all goods, greater scarcity leads a greater price, and then the interest rate, or the price of borrowing money, rises.

- An increase in the amount of available loanable funds means that there are more people who want to lend. They, therefore, bid the price of borrowing (the interest rate) downwardly.

Source: https://opentextbc.ca/principlesofeconomics/chapter/28-4-monetary-policy-and-economic-outcomes/

Posted by: smithprame1944.blogspot.com

0 Response to "What Does A Change In Monetary Policy Affect"

Post a Comment